The world continues to produce gold and silver. Central banks are increasing their gold purchases. Industrial demand for silver is reaching record levels. Yet there is a critical reality on the mining side that often goes unnoticed:

Beneath the ground, new large deposits are no longer being found as they once were.

This situation is not only about prices; it points directly to a geological and physical tightening of supply.

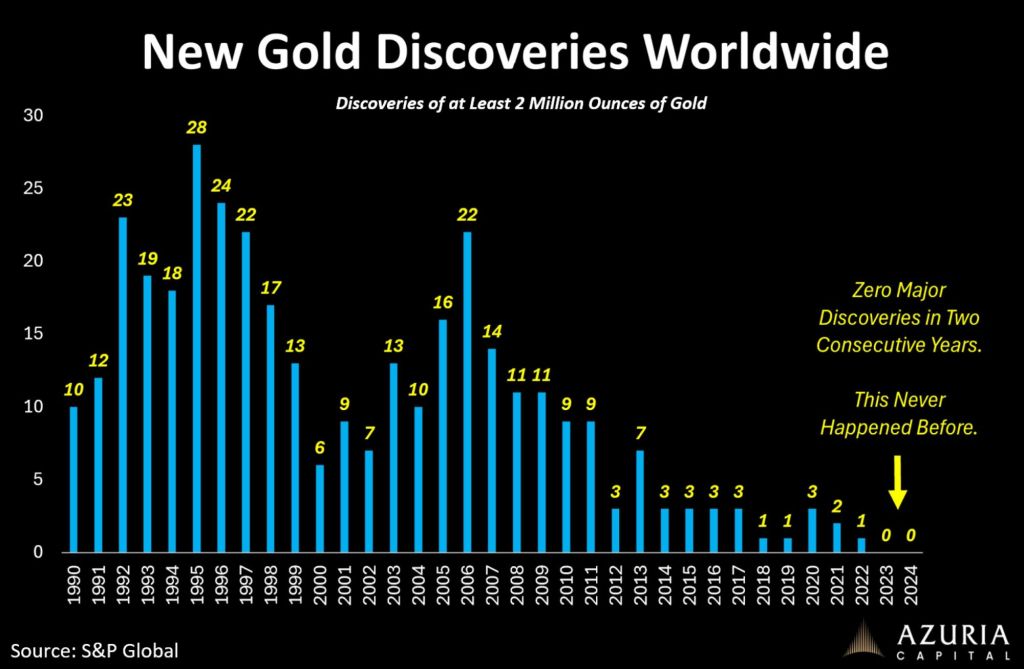

Institutions such as S&P Global define a “major discovery” as a new deposit containing at least 2 million ounces of gold that is economically viable to extract. During the 1990s and early 2000s, dozens of such discoveries were made every year. In recent years, however, this number has declined dramatically. In fact, in some recent years, not a single new major gold discovery has been recorded worldwide. This is not a normal situation in mining history.

There are several key reasons for this. The easy-to-find, high-grade, near-surface deposits have largely already been discovered and mined. New discoveries are now deeper, lower grade, and far more expensive to develop. Mining companies have reduced exploration budgets and are focusing instead on expanding existing sites. In addition, environmental and political barriers have made it much more difficult to bring a newly discovered deposit into production.

Today, when discussing gold and silver prices, attention is usually focused on interest rates, the dollar, geopolitical risks, and inflation. However, the real long-term story is being written on the supply side. Because without discoveries, there is no future production.

Gold production continues based on existing reserves. But if new reserves are not added, natural supply constraints will begin to appear in the coming years. The situation is even more critical for silver. Silver is heavily used in solar panels, electronics, defense industries, and electric vehicles, and its recycling rate is limited.

This is not a financial bubble or speculation. It is a geological reality. The long-term direction of gold and silver prices will be shaped not only by central banks, but by geology itself.

While the world continues to consume gold and silver, it is failing to find new large deposits. This quiet development is one of the most important factors explaining why commodity prices may remain structurally strong in the years ahead.

Gold and silver are no longer only financial safe havens; they are also becoming physically scarcer assets. And this process is only just beginning.

Yorum bırakın